NET UNREALIZED APPRECIATION (NUA)

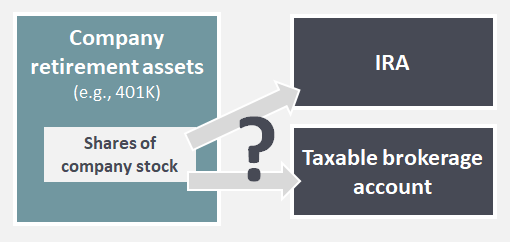

Net unrealized appreciation (NUA) refers to an IRS provision regarding company stock inside a retirement plan. If you have come to this page to learn about NUA, then you are probably facing an important but potentially challenging decision. In particular, you may be investigating whether you should distribute some or all of these securities in-kind.

This approach may provide tax advantages. That is, the NUA will ultimately be taxed as a long-term capital gain rather than as ordinary income. However, it may also leave you with concentrated risk in your company's stock.

Alternatively, you may have the option to roll these shares over into an IRA. This approach allows for diversification into other investments. However, these funds will ultimately be taxed as ordinary income upon distribution.

One must weigh the tax benefits against the investment (i.e., concentration risk) considerations. Only then can one sensibly decide what to do with shares of stock in your company's retirement plan.

The Stakes Are High

NET UNREALIZED APPRECIATION (NUA) DIAGRAM

For those with significant company stock holdings, NUA is naturally a more critical decision worth taking the time to analyze. Moreover, this is a very nuanced decision. So it should not be taken lightly or based on rules of thumb. Indeed, there are many variables that go into this decision and they are different for everyone. Some of these include:

- Income tax rate (current and future)

- Capital gains and dividend tax rates

- Diversification/concentration preferences

- Estate size

- Long-term plans for these assets (e.g., spend versus pass onto heirs or charity)

- The fundamental quality of your company (will it be around in 10, 20, or more years?)

- Sentimental attachment to the company

- Your life expectancy

- Beneficiary plans for these assets if inherited (i.e., spend or maximize tax benefits)

Beware of Flawed NUA Models

In the process of helping my clients with their NUA decisions, I looked for resources to help me make some relevant calculations and weigh various options. However, the online NUA tools I came across were inadequate for multiple reasons. In particular, their models embedded erroneous assumptions and overlooked significant details.

In some cases, they naively compared the total amount of taxes paid for the NUA versus an IRA rollover option. However, minimizing taxes paid is not the same as maximizing after-tax returns or wealth. For example, consider the IRA rollover option. Only looking at the taxes one pays completely ignores the benefits provided by IRA accounts. However, some of these benefits are significant and can extend beyond the original owner's lifetime (i.e., via inherited IRAs). I provide a more technical accounting of the math behind the benefits of retirement accounts in my article Quantifying the Value of Retirement Accounts. Moreover, my follow-up article Illustrating the Value of Retirement Accounts provides more user-friendly examples.

A Better NUA Calculator

Given these issues with existing tools, I decided to build my own model. My goal was to provide a more accurate and comprehensive analysis. You can find my free online NUA tool at www.NUAcalc.com. I made this tool for roll-up-your-sleeves DIY individuals and professional advisors dealing with NUA options. If that is you, then I hope it can help you make better decisions. If that is not you and you would like specific advice regarding NUA or other investment-related matters, please get in touch (details on my contact page).

Please note: I have not updated this tool after the passing of the 2017 Tax Cuts and Jobs Act (TCJA). However, you can customize the inputs to reflect the shortening of 'stretch' options.

You may also learn more about me and my firm here: