| "Nothing in life is to be feared. It is only to be understood.” – Marie Curie |

| “You get recessions, you have stock market declines. If you don't understand that's going to happen, then you're not ready, you won't do well in the markets.” – Peter Lynch |

| “Successful investing is about managing risk, not avoiding it.” – Benjamin Graham |

| Many investors think of bonds as a diversifying asset for their portfolios. In particular, they use bonds to help combat stock market volatility. Many financial advisors happily accommodate (if not promote) this fear of stock volatility and advocate 60/40[1] or similar portfolios with their clients as representing a reasonable balance of risk and return.

Academic and practitioner research further supports this “asset allocation” approach. Indeed, there are many studies highlighting 90% of portfolio returns are determined by asset allocations. Accordingly, it is not surprising how prevalent this asset allocation model is with investors of all types. This article analyzes the assumptions behind asset allocation models. We revisit both the purpose (risk reduction) and performance (returns) of standard asset allocation approaches relative to some alternative strategies. We also discuss the flawed logic behind using the 90% explanatory statistic above to support the use of asset allocation models. At the heart of this paper is the notion of risk. Like Warren Buffett, we find the conventional definition of risk most academics and practitioners use (i.e., volatility or standard deviation of market returns) is inappropriate. Accordingly, strategies that minimize this ill-defined risk metric may not be optimal. Indeed, we show how the mechanics of asset allocation strategies can systematically constrain performance and dampen long-term returns. Investors who attain a better understanding of the real risks associated with stock investing (as well as the true cost of avoiding ill-defined risk) may wish to construct their portfolios differently (spoiler: higher equity allocations). This can enable them to significantly outperform 60/40 and similar benchmarks over the long term. To be sure, the views on risk we share here are not new or innovative. We are merely reiterating ideas Buffett and other great investors have advocated for years. |

Figure 1: Example Asset Allocations (stock % / bond %)

| Nervous Nelly (80/20)

|

Middle of the Road (60/40)

|

Warren Buffett (100% equity)

|

Source: Aaron Brask Capital

Asset Allocation Defined

Asset allocation refers to the process by which an investor or investment professional allocates percentages of a portfolio amongst various asset classes (e.g., stocks, bonds, real estate, commodities, etc.). For example, a 60/40 portfolio is one in which 60% of the assets are allocated to stocks and 40% to bonds. For the purpose of simplicity, we will confine our discussion to just these two asset classes.

The logic behind the asset allocation process revolves around diversification and risk. Stock prices typically fluctuate more than bonds and this volatility makes many investors uneasy. In addition to bonds typically being less volatile, they often move in the opposite direction over shorter periods thereby offsetting portfolio volatility even more. Given few if any investors enjoy wild swings or deep drawdowns in their portfolio value, divvying up portfolios between stocks and bonds seems a sensible approach to reduce unwanted volatility.

The discomfort associated with market volatility is one reason investors like to reduce portfolio volatility. However, there is another and perhaps more important reason. It relates to investors’ emotional or behavioral reactions to this discomfort and the corresponding impact on investment performance. For example, after markets rise and seemingly only go up, investor sentiment is high and many investors take on more risk in their portfolios. Moreover, after markets have fallen and market prices are depressed, negative sentiment abounds and many investors cut their losses and move to the sidelines.

Unfortunately, these reactions occur after markets have already moved and the typical result is a buy-high/sell-low strategy. This is a recipe for dismal investment performance. In this light, reducing the volatility of one’s portfolio can help avoid these temptations and performance-dampening decisions.

| Note: We do not discuss them in this article but there are also more advanced implementations of asset allocation. Amongst these alternatives, risk parity is probably the most popular. In a risk-parity allocation, investment positions are formulated based on risk allocations instead of dollars. For example, a standard 50/50 asset allocation would translate into an equal amount of dollars invested in each of the stock and bond allocations. However, a 50/50 allocation within a risk parity portfolio would mean that the amount of risk emanating from the stock portfolio would be the same as from the bond portfolio. So if the risk for stocks was +/-15% and +/-5% for bonds, then the bond portfolio would be three times (15% ÷ 5%) the dollar size of the stock portfolio in order to equate the risks (i.e., risk parity). |

Asset Allocation Details

Asset allocation strategies vary in multiple dimensions. The first and most obvious variation related to how much (if any) to allocate to various asset classes. In general, investors with longer time horizons and higher appetites for risk will allocate higher percentages to stocks.

The percentage allocations may be static or dynamic through time. In our experience, most investors prefer to determine a static asset allocation and stick to it through thick and thin. Other investors prefer an approach whereby they specify ranges instead of precise levels. This allows their investment managers to exploit tactical strategies to take advantage of potential market opportunities (e.g., increasing the allocation to stocks when they are priced more attractively than bonds). Alternatively, some investors prefer to revisit and dynamically set the allocations based on their own requirements or market perceptions.

Another important detail relates to how often asset allocations are brought back within their required ranges. Many investors follow a time-based approach whereby allocations are adjusted, say, quarterly or annually. Other investors employ thresholds or buffers to trigger rebalancing. That is, if the maximum allocation for equities is 60% then they may wait until the allocation exceeds that level by a buffer – typically between 0% and 5%. Furthermore, some may wait until this buffer is exceeded for a minimum amount of time (e.g. two consecutive monthly readings). Approaches like this can be used to reduce trading (and potential capital gains taxes) by ignoring small or temporary breaches of the prescribed limits.

Three Issues with Traditional Asset Allocation Strategies

While all of the above strategies may sound sensible, there are some holes in the logic. This section highlights three issues with traditional asset allocation strategies we find are rarely discussed by investors or advisors. The first issue relates to how risk is defined. Given the overall goal of diversifying via asset allocation is to reduce risk, it is vital to understand the definition of risk. While statistical formulas based on market prices may be academically elegant and easy to compute, it is more important to utilize a definition that accurately reflects the risk investors actually experience.

The second issue relates to the logic and statistics used to advocate asset allocation models. We debunk two popular arguments used to make the case for using these models. The first claim involves a commonly cited statistic from a 1986 article published in the Financial Analysts Journal entitled “Determinants of Portfolio Performance”. In this article, the authors (Brinson, Beebower, and Hood) claimed more than 90% of portfolio variation is explained by asset allocation. While we agree with this conclusion, their findings have been both misquoted and misinterpreted on many occasions in an effort to advocate asset allocation strategies and discredit more active approaches. However, these assertions are not supported by the above statistic or the paper from which it originated.

The benefits of asset allocation (risk reduction) are well-known and often discussed. However, the real price investors pay for diversifying their portfolios via asset allocation strategies is not. That is the subject of the third issue we highlight. Over the long term, equity allocations have outperformed bonds and most (including us) expect this to be the case going forward. Accordingly, taking money from stocks and allocating it to bonds will likely translate into lower long term performance. We point out just how much performance investors might be missing out on so they can weigh the costs against the benefits for asset allocation strategies.

Issue #1: Risk Is Not the Same as Volatility

| “In investing, what is comfortable is rarely profitable.”

– Rob Arnott (CEO of Research Affiliates) “Finance departments believe that volatility equals risk. They want to measure risk, and they don't know how to do it, basically. So they said volatility measures risk.” – Warren Buffett (1997 Berkshire annual meeting) “Risk had a very good colloquial meaning, meaning a substantial chance that something could go horribly wrong, and the finance professors sort of got volatility mixed up with a bunch of foolish mathematics and to me it's less rational than what we do.” – Charlie Munger (1997 Berkshire annual meeting) |

The most common measurement of risk used by investors and investment professionals is volatility. Mathematically, volatility is the annualized standard deviation of price returns. Like many legendary investors including Warren Buffett and his partner Charlie Munger, we feel the common characterization of risk as volatility does not accurately reflect the true nature of investment risk experienced by investors.

There are many problems with using this statistical formula for volatility to define risk. We highlight three here:

- Ignores fundamentals: Volatility only reflects the behavior of market prices and there is significant noise in market prices. It does not consider the quality of the underlying businesses nor the prices at which they are owned (valuation in particular).

- Short term focus: Volatility typically emphasizes short-term focus as it is often calculated over periods of one year or less. Unfortunately, there is significant noise in market prices over shorter periods we cannot control.

- Backward looking: In addition to the short-term nature of the calculation, another issue we have with this definition of risk is that it is backward-looking; volatility is calculated using historical market prices. Accordingly, there is little that speaks to the future risks investors might experience.

| Geek’s Note

The formula for volatility is: where ri are the individual returns and ru is the average. |

| It is interesting to note the volatility formula systematically removes (subtracts) the average return from each individual return. We believe the average return, if anything, is actually the most relevant information used in this calculation. If the period over which it is calculated is long enough, the average return could be indicative of future returns (to the extent fundamentals are persistent and prices follow fundamentals). If the period is not long enough to compute a meaningful return, then calculating and observing deviations from this return over much shorter periods will yield even less meaningful information.

|

In reality, short term market fluctuations do not represent real risk to investors unless they extract money. If one does not need to extract capital from their investments, then this definition of risk relates more to the danger of reacting to this perceived risk in a sub-optimal manner. For example, one does not need to liquidate or raise cash but exits the market due to uncomfortable market volatility or drawdowns.

Given the excessive focus on market price movements by the media and investment industry, we advocate two methods for dealing with this perceived risk:

- We encourage investors to focus more on fundamental performance rather than market performance. As we discuss later, fundamental performance is generally more stable than market prices. In fact, we have developed our reporting software specifically dedicated to this purpose. Please visit www.FundamentalReporting.com for more information.

- We also encourage investors to integrate quality and value into their equity portfolios. Higher quality companies can weather economic storms better than lower quality companies. Moreover, stocks with lower valuations can mitigate the downside risk of valuation changes versus glamour stocks with lofty valuations which may be more vulnerable contracting valuations.

| A Real Estate Analogy

Many people own real estate as an investment because they feel it is more tangible; they can understand and manage it without too much uncertainty. As long as the rent checks keep coming in and rising over time, many real estate investors are not overly concerned with the precise value of their properties. Indeed, property values are rarely appraised aside from the time they are purchased or sold. We encourage investors in stocks to treat their investments the same way – less focus on prices. However, technology and media constantly push so much stock price data around it is hard to ignore. Prices may go up and down significantly, but it does not mean you have to act. |

Most investment professionals and investors focus on longer term goals over horizons of 5, 10, 20, or more years. Accordingly, discussions or measurements of risk should correspond to the feasibility of achieving those longer term goals and not the short term noise. A major factor that may dictate the feasibility of various goals is the longer term performance of stocks – will they deliver adequate returns over time? Not everyone has the same level of confidence in the markets or the fundamentals behind them.

“In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.”

|

One step toward having more faith in markets (i.e., their ability to deliver returns over the longer term) is to understand markets better and monitor more than just market prices. Unfortunately, the financial services industry broadly encourages what we call the squiggly line perception of markets. Indeed, many investors think of the stock market as nothing but random squiggly lines on charts that could go up or down at any point. This perception only encourages the use of naïve statistical formulas to define risk.

As highlighted above, the fundamentals get lost with the above view of markets. This is important because the fundamental performance underlying the companies in the market is not nearly as volatile as the market. Whether one looks are dividends, book value, or other fundamentals, it becomes clear that markets themselves are a source of volatility above and beyond the volatility of the fundamentals. Indeed, investments traded in the market are subject to the often-emotional biases of investors and market prices can deviate significantly from the fundamentals in the short term.

Over the longer term the prices follow the fundamentals. While there is always disagreement about what the precise price for an investment (e.g., a stock) should be, investors are constantly combing the markets looking for bargains (and opportunities to short) and this helps align prices with fundamentals and make markets relatively efficient. The bottom line is that we believe that monitoring fundamental performance is just as if not more important than market price performance.

More generally, we like to break market prices down into two components – fundamentals and valuations. In particular, the price of an individual company depends on its fundamentals and the valuation the market attaches to those fundamentals. Mathematically speaking, the price P of a company can be expressed as P = F x P/F where F is a fundamental quantity (e.g., book value or earnings), so P/F is a valuation metric (e.g., Price-to-book to Price-to-earnings ratio).

The returns investors experience with the overall market (or individual investments) can be directly attributed to the performance of the underlying fundamentals and the changes in valuations. It really is just basic math. We believe this decomposition can help investors better understand the nature of the risks associated with investing in stocks by helping them separate the fundamental performance from the noise introduced by the markets (e.g., ever-changing valuations).

| Two Corollaries

We derive two corollaries from our simple market price model (P = F x P/F). The first is to invest in enterprises with solid, growing fundamentals (a.k.a. quality investing). The second is to invest when valuations are attractive (a.k.a. value investing). It is just math; growing fundamentals (F) and valuation (P/F) expansion are the only two ways the stock price (P) can increase. Unfortunately, these corollaries are not without controversy. Many academics and practitioners dogmatically adhere to the efficient markets hypothesis. They claim efforts devoted to identifying high quality companies or those trading at attractive valuations are futile. In other words, they believe Warren Buffett, Peter Lynch, and other great investors of our era were just lucky. We beg to differ[2]. There is much empirical evidence indicating the benefits of integrating quality and value into an investment framework. It is worth noting these attributes can be assessed on both a cross-sectional and temporal basis. We will not regurgitate all of the details here, but our Index Investing: Low Fees but High Costs article describes how quality and value metrics can be used in the context of (cross-sectional) security selection to outperform standard market portfolios. Moreover, our More Market Correction to Come article explains how overall market valuations correlate strongly to subsequent (long-term) market returns and how investors can enhance performance by adjusting their market exposures on the rare occasions when the overall market is extremely over- or under-valued[3]. |

The point of the above corollaries is not necessarily to advocate the use of value and quality[4] (admittedly, it is an ancillary motive!). Our goal is to point out there are better ways to monitor risk than looking at historical volatility. Focusing on market prices and statistics derived from them shed little light on future risks. Regardless of whether one elects to integrate quality and value into their decisions to buy and sell investment, we believe these metrics provide a much better indication of forward-looking investment risk than backward-looking volatility-based figures.

More generally, we believe one should focus on longer-term goals and the risks that affect the likelihood of achieving them. In our view, analyzing risk for longer term goals requires five key components:

- Sound models based on conservative assumptions regarding future market performance

- Setting realistic goals relative to one’s resources

- Formulating an investment strategy to minimize real risk to one’s goals. We generally define real risk as permanent loss of capital (not a temporary market downturn). Permanent loss of capital could result from investing in a business that fails or overpaying for an investment.

- Executing the investment strategy with discipline to avoid strategic risks (e.g., getting nervous and selling during or after a market downturn).

- Monitoring and re-evaluating models, assumptions, and feasibility of goals.

The entire process of analyzing risk for longer-term goals relies on models for estimating a realistic probability for achieving one’s goals. Calculating this particular figure is critical to the rest of the planning process as well as to the execution of the corresponding investment strategy. However, we find the models offered by most advisors rely far too much on volatility-based statistics and other noisy market data. We discuss the issues with these models and highlight potential solutions in our article Destroying Steady Income. Please contact us to request a copy of this article or discuss how these issues related to your investment process.

| Volatility Anecdotes

Is it sensible to travel by car from Miami to San Francisco in order to minimize the exposure to turbulence? Avoid vaccinations due to fear of getting pricked by a needle? We may not like some things but it is important to view the bigger picture and not let ourselves get paralyzed by misguided notions of risk. Sure, market volatility is something few investors enjoy (some actually do enjoy it!). However, if one understands downswings are only temporary and is confident they will be rewarded over the long term, then they should be better-prepared to tolerate it. |

Issue #2: Flawed Logic and False Claims

In 1986, three academics (Brinson, Hood, and Beebower a.k.a. “BHB”) published an oft-cited paper entitled “The Determinants of Portfolio Performance” in which the authors boasted of their “striking” findings whereby asset allocation accounted for 93.6% of the total variation in pension plan returns. They followed up with an updated study just over a decade later. This study essentially reconfirmed their earlier results by calculating a similar figure (91.5%) with more recent data. Based on these findings, many academics and practitioners started to advocate static asset allocation strategies based on passive investments.

To be clear, we do not disagree with the calculation of this statistic; we emphatically disagree with using their statistical findings to advocate static asset allocation strategies. For starters, concluding that asset allocation has a large impact on performance in no way indicates asset allocations should be fixed through time. There is a gap in the logic to arrive at the latter assertion. Indeed, we could argue that because asset allocation is so important, it deserves more attention and adjustment through time.

The authors’ claim that their results are “striking” is naïve at best. What their paper is really just pointing out is that asset classes are very different and generate different returns. For example, let us compare security selection to asset allocation. If one sells a particular tech stock and buys another in the same sector, not that much has changed. The resulting impact on overall performance will not move the dial much. However, if one reallocates money from a tech stock over to a treasury bond, then the impact will typically be much more significant. These 90%+ statistics are really just saying stocks are different than bonds.

Consider a relay race around a large track with 10 legs. Each contestant gets to choose between various models of motorcycles and cars for each leg. For those who do not know, motorcycles are typically much faster than cars. Is it really surprising the types of vehicles (motorcycles versus cars) turns out to be much more important in determining who wins most races relative to which model of motorcycle or car is chosen? We could perform a similar study to BHB’s portfolio analysis and would probably find 90% or more of races were determined by the types of vehicles chosen.

| Geek’s Note

Statistically speaking, 93.6% and 91.5% (out of 100%) are certainly significant figures. However, it is critical to realize these figures refer to the variation (or volatility) of returns – not the absolute level of returns achieved. By analyzing variation of returns instead of the absolute level of returns themselves, the authors have effectively ignored the end result (terminal wealth) that we believe ultimately matters. This notion was pointed out by William Jahnke in his 1997 paper entitled “The Asset Allocation Hoax”. In his conclusion, Jahnke stated: “…agreement that asset allocation is important does not settle the issue of how to do it. What are the appropriate asset classes? Should asset class weights be fixed or dynamic? How should asset allocation be determined? What about the cost of implementation?” |

Given the above gaps in logic, why do so many follow this fixed asset allocation model? We believe some of the reason stems from the academic elegance. We find academics tend to gravitate toward theories where they can make use of the vast amount of market price data available. Despite the logical flaws, the aesthetics of the formulas and output are too much to resist.

On the practitioner side, the fixed asset allocation model makes life easy. It is very practical for advisors and the institutional investment consultants. First, the idea already has plenty of momentum and is often considered industry standard. No one ever got fired for buying IBM! Effectiveness aside, this model is also very well-defined, easy to explain, and simple to execute. Moreover, it creates the illusion of work even though many firms now offer robo-rebalancing for free. These attributes make this model both very marketable and defensible. This latter point should not be underestimated. Indeed, alternative strategies might be considered too aggressive and create liability. Moreover, going against the grain requires educating clients on and coaching clients through inevitable periods when the performance lags fixed allocation portfolios and they feel like they are missing out.

Imposing fixed asset allocation models on investors relieves advisors and investment consultants of asset allocation decisions. In Jahnke’s words, this approach “conveniently shelters both the consultant and the investment manager from the most important investment decision.” In our experience, we rarely come across an investor, advisor, or consultant that does not assume fixed asset allocations are a given.

| Security Selection and Market Timing

The strategies we discuss in this article operate independent of market valuations. We use the S&P 500 as a proxy for the US stock market on a buy-and-hold basis. That is, our discussions and analysis do not attempt to integrate security selection or market timing. Notwithstanding, we believe using valuations can significantly improve investment performance both cross-sectionally (i.e., security selection) and temporally (i.e., market timing). Notwithstanding, one must consider investor risk profiles, the impact of taxes, transaction costs, and other factors when determining the utility such strategies. We find many practitioners use valuations for security selection but not for market timing. Indeed, market timing is generally considered blasphemy amongst market professionals. While we acknowledge such a strategy is not suitable for all investors, we disagree with the stigma attached to market timing. For bonds, valuations are just basic math. If one knows the price of a bond and its cash flows, then calculating the yield or return is straightforward. In particular, more attractive valuations (i.e., higher yields) directly and mathematically result in higher returns (assuming a buy-and-hold strategy with no defaults). For stocks, the cash flows and fundamentals are less certain. Moreover, there is much noise in the relationship between fundamentals and market prices (i.e., valuations). There is a long list of valuation models but, unfortunately, many of these models to do not accurately relate the fundamentals to the market prices. Our market valuation model is more robust. Even Warren Buffett has acknowledged the type of valuation model we use is “probably the best single measure of where valuations stand at any given moment”. More importantly, our core valuation model has a 90% correlation with actual market returns – a feature many of the intuitive sounding but flawed valuations models lack. We believe sensibly integrating valuations can help you increase your returns. Our articles Index Investing: Low Fees but High Costs and More Market Correction to Come provide detailed discussions of how valuations can improve both security selection and market timing, respectively. |

Issue #3: The Real Cost of Diversifying

The first two issues above highlighted logical flaws embedded in many asset allocation models. Indeed, we believe investors should measure and manage risk differently. Despite these shortcomings, we acknowledge asset allocation strategies still address a known problem (however misguided) many investors face by imposing diversification at the asset class level to reduce the perceived market price volatility of portfolios. The point of this section is to estimate the costs borne out of this diversification.

One of the primary assumptions made with virtually every asset allocation strategy is that stocks outperform bonds over the long run – hence the typically larger allocations to stocks (e.g., 60 versus 40). Given this assumption (which we agree with and discuss in the shaded section below), it follows that making allocations to bonds will reduce overall portfolio returns relative to stocks. We examine the magnitude of this impact by comparing returns from various stock and bond allocations.

| Why Stocks Generate Higher Returns

The conventional wisdom is that stocks go up more than bonds over the long-term. This has certainly been the case historically, but will it persist? Our view is that it will. In addition to the historical record, we base our opinion on three factors. The first factor is simple: Bonds are fixed income investments. Their principal does not grow as the value of a bond does not exceed the sum of its par value and coupons. The second factor is that investors are generally averse to volatility and thus require a discount to purchase stocks relative to more stable bonds. This discount (sometimes referred to as the equity premium) translates into higher subsequent returns. In our view, it is not volatility itself that creates this discount (otherwise, the same logic would apply to shorting stocks as well); it is the timing of the volatility. In particular, stocks prices tend to fall during economically challenging times when there is strong demand for liquid capital. In other words, stocks are least liquid when opportunities to deploy capital profitably abound. The third factor relates to the corporate perspective. When companies borrow money via loans or issuing bonds, they must manage their finances as to repay the interest and principal. These liabilities impose significant financial constraints on a company. Issuing equity places no such financial constraints. Accordingly, there is a liquidity preference for issuing equity and corporates thus have incentive to price it more favorably to entice investors. Of course there are occasional shorter periods when bonds outperform stocks. Moreover, there will always be individual cases where some bonds outperform some. However, we believe these three factors are not likely to go away and will sustain the long term outperformance of stocks over bonds. |

Historical Performance of Stocks versus bonds

We first estimate the costs of allocating money to bonds versus stocks by looking at historical performance. We compare the performance of five different portfolios ranging from all stocks to all bonds. We use the S&P 500 index as a proxy for stocks and the 10-year treasury as a proxy for bonds. The asset allocations we use are: 0/100, 25/75, 50/50, 75/25, and 100/0 (% stocks / % bonds).

Our data source goes back to 1972. The first table shows performance over the entire period. We then decompose this period into two smaller periods from 1972-1982 and 1982-2015. Notably, interest rates were generally rising over those first 10 years and falling during the latter period.

The reason for looking at these smaller periods is two-fold. First, we believe the first period of rising rates may be more relevant going forward given the current low level of interest rates. Second, we believe the latter period should be the most conservative period over which to compare stocks and bond performance. In particular, declining interest rates provide a direct, mathematical tailwind for the performance of bonds. That is not to say declining rates to do also help stocks. However, we believe this trend favors bonds on balance.

Figure 2: Asset Allocation (stock % / bond %) Performance From 1972-2015

| Portfolio | Stocks | Bonds | CAGR | Terminal Wealth | TW versus 100% Bond |

| 0/100 | 0 | 100 | 7.1% | $202,463 | 100% |

| 25/75 | 25 | 75 | 8.2% | $321,639 | 159% |

| 50/50 | 50 | 50 | 9.1% | $460,749 | 228% |

| 75/25 | 75 | 25 | 9.7% | $593,835 | 293% |

| 100/0 | 100 | 0 | 10.1% | $682,712 | 337% |

Source: Aaron Brask Capital, PortfolioVisualizer.com

The overall results for the entire period are in the above table. There was a +3% return advantage for investing in stocks versus bonds. Given the length of the period (43 years), stocks generated vastly greater terminal wealth – 3.37 times as much versus investing in bonds alone.

Looking at the initial decade from 1972-1982 where interest rates were rising, the absolute level of returns was lower as was the additional return from stocks at +1.7%. Based on the lower overall returns and the shorter period, investing in stocks yielded just under 20% more terminal wealth overall. While these results occurred over a 10 year period, we can extrapolate this trend over a 43 year period to compare with the terminal wealth above. In this hypothetical case, stocks would result in over 2 times as much wealth as investing in bonds.

Figure 3: Asset Allocation (stock % / bond %) Performance From 1972-1982

| Portfolio | Stocks | Bonds | CAGR | Terminal Wealth | TW versus 100% Bond |

| 0/100 | 0 | 100 | 5.7% | $18,423 | 100% |

| 25/75 | 25 | 75 | 6.5% | $19,982 | 108% |

| 50/50 | 50 | 50 | 7.0% | $21,116 | 115% |

| 75/25 | 75 | 25 | 7.3% | $21,756 | 118% |

| 100/0 | 100 | 0 | 7.4% | $21,854 | 119% |

Source: Aaron Brask Capital, PortfolioVisualizer.com

The table below looks at the rest of the period from 1982-2015 where interest rates were falling, the absolute level of returns was higher and the additional return from investing in stocks relative to bonds was +3.1%. In other words, investing in stocks yielded more than 2.5 times as much terminal wealth versus investing in bonds. Extrapolating this trend over a 43 year period indicates stocks would result in over 3.4 times as much wealth as investing in bonds alone.

Figure 4: Asset Allocation (stock % / bond %) Performance since 1982-2015

| Portfolio | Stocks | Bonds | CAGR | Terminal Wealth | TW versus 100% Bond |

| 0/100 | 0 | 100 | 8.2% | $145,950 | 100% |

| 25/75 | 25 | 75 | 9.3% | $208,984 | 143% |

| 50/50 | 50 | 50 | 10.3% | $276,800 | 190% |

| 75/25 | 75 | 25 | 10.9% | $338,132 | 232% |

| 100/0 | 100 | 0 | 11.3% | $377,688 | 259% |

Source: Aaron Brask Capital, PortfolioVisualizer.com

For readers interested in a longer historical comparison (that essentially arrives at the same conclusion), we recommend the book Triumph of the Optimists by Dimson, Marsh, and Staunton. They review over 100 years of data on stock and bonds performance. Moreover, they broaden their study to include markets from 16 countries in total.

Model-based Projections of Stocks versus Bonds

The second way we compare the performance of stocks to bonds is by modeling various scenarios. We use a 20 year period for analysis. This provides sufficient time for any difference in return to compound and manifest itself. It is also a reasonable time frame over which many investors might consider for wealth accumulation or de-cumulation (i.e., retirement).

We model bonds in a straightforward manner by calculating an internal rate of return (IRR) based on the cash flows of each hypothetical bond. We assume bonds are trading at par and consider various levels for interest rates or yields. The initial cash outflow is $1,000 as is the repaid notional at maturity. Interest is paid in equal installments annually. Note: Implicit in this is the assumption of no defaults which we find reasonable for investment-grade bonds.

Our model for the stock portfolio is essentially the same except the cash flows (i.e., the amount of dividends or the value of the portfolio at the end) are not known in advance. Accordingly, we present several scenarios we believe to be reasonable. We make varying assumptions for the initial levels and growth of the fundamentals (i.e. earnings, book value, and dividends) and valuations.

We analyze the impact of taxes for both stocks and bonds. This includes interest being taxed as ordinary income as well as variable rates for dividends and capital appreciation should assets be liquidated at the end of the period.

In a nutshell, the moving parts or variable inputs for our model are as follows: interest rates, initial and terminal stock valuations, initial dividend yield, fundamental growth rate, and tax rates (dividends, long term capital gains, and income). A few notes about our variables:

- We do not include terminal levels for interest rates because we are assuming each bond is held to maturity (at which point the interest rate is irrelevant). While fixed maturity exposures are popular in practice, we do not model them for two reasons. First, it requires buying and selling bonds throughout the period and this significantly complicates the calculations for bond income, principal, and the corresponding taxation. The second and perhaps more important reason is we believe buying and selling bonds before maturity contributes unnecessary volatility to the portfolio and income stream. Indeed, the sanctity of bonds as fixed income investments is built around the notion that investors get their principal back at maturity. If a bond is not held to maturity, then this key benefit is destroyed.

- We do not specifically identify different types of bonds. However, the range of interest rates implicitly covers a wide variety of bonds. This includes municipal bonds as well since their rates can be converted to tax-equivalent yields (i.e., the equivalent level of pre-tax yield that would result in their tax-free yield).

- We do not specify a terminal dividend yield as it is implied by the initial dividend yield and fundamental growth rate.

Given the dimensionality of the inputs, we do not present the results for all possible combinations. We selected what we believe to be representative and relevant scenarios for investors given current market levels. In particular, we chose three scenarios we believe to be conservative, balanced, and optimistic with regard to comparing the performance of stocks to bonds.

Figure 5: Stocks versus Bonds – Model Assumptions and Results

| Assumptions | 20yr rate | Valuation

(initial / terminal) |

Dividend yield | Fundamental

Growth Rate |

Taxes

(div / LTCG / income) |

Performance

Stocks Bonds |

|

| Conservative | 5% | 20 / 10 | 2.5% | 4.0% | 40% / 30% / 40% | 2.5% | 3.0% |

| Balanced | 4% | 20 / 15 | 3.0% | 5.5% | 30% / 20% / 40% | 6.0% | 2.4% |

| Optimistic | 3% | 20 / 15 | 3.0% | 7.0% | 20% / 20% / 40% | 7.7% | 1.8% |

Source: Aaron Brask Capital

Note: Please feel free to contact us if you would like us to simulate a different scenario. Alternatively, if you would like to make your own comparisons, just request a copy of our spreadsheet model (which also includes a separate comparison of real estate).

While we used the labels, conservative, balanced, and optimistic, we believe our assumptions for stocks were conservative overall. Indeed, even during the period from 1972-1982 when interest rates more than doubled and exceeded 14% while valuations halved, the fundamentals grew more than 8% annualized. Moreover, our model assumed the stock portfolio was liquidated at the end of the period and subject to capital gains taxes.

The reason we chose such conservative assumptions was to evidence just how pessimistic one must be in order to expect bonds to outperform stocks. Based on even our most pessimistic assumptions including 4% growth rates and a halving of market valuations, our calculations indicate bonds would only slightly outperform stocks (3% vs 2.5%).

It is also worth noting we used the S&P 500 as our proxy for stocks. This index embeds no risk management other than diversification. However, even that benefit is diminished due to the market capitalization weighting which makes the index top-heavy. We believe careful screening for quality and value translates into better stock performance. Avoiding lower quality businesses and selecting those with higher and more robust growth can increase the over fundamental growth. Moreover, purchasing these companies at fair to attractive valuations can augment returns further. Our research article Index Investing: Low Costs but High Fees provides a more in-depth discussion of quality and value as they relate to portfolio performance. We explain the logic, highlight relevant research, and provide historical evidence.

Our ultimate point with the above performance data is to emphasize the significant performance differential between stocks and bonds. This data illustrates the real cost of allocating money to bonds. Of course, investors might experience more volatility with higher allocations to stocks. However, we do not believe that is indicative to real risk.

In our view, the real cost of investing in the stock market is the potential lack of liquidity. The liquidity risk we are referring to is not the ability to sell stocks and raise cash; it is about the ability to sell at reasonable prices. While stocks can generally be bought and sold with minimal market impact or transaction fees, their prices sometimes remain depressed for extended periods during market corrections. During these periods it is typically unwise to sell and lock in unnecessary losses. As such, an investor’s time horizon must be long enough to ride out potential market volatility.

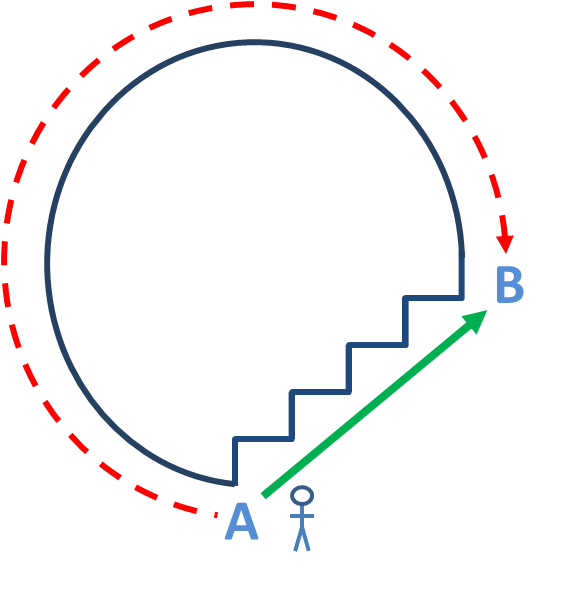

| Volatility Analogy

Another way to think about the relationship between volatility and returns is illustrated below. There are two paths for one who wants to walk from point A to point B. One is longer and smoother; the other is shorter but zigzagged. If one does not like changing directions, then they might opt for the smoother but longer path.

|

Assuming they would walk at the same speed, the smoother path would take approximately three times longer to arrive at point B. The point here is that imposing constraints can limit efficiency. One should consider the broader situation and implications, not just their preferences.

Assuming they would walk at the same speed, the smoother path would take approximately three times longer to arrive at point B. The point here is that imposing constraints can limit efficiency. One should consider the broader situation and implications, not just their preferences.Conclusions

| Note: It is worth stressing this discussion is relevant to investors with longer time horizons (e.g., 10 years or greater). For investors with shorter horizons, it is critical to align assets with liabilities. If you are planning on purchasing a house next week, it is generally not be sensible to invest the funds in the stock market as the value could fluctuate significantly in a week’s time. |

This article has demonstrated at least three major issues with traditional asset allocation strategies (misguided definitions of risk, flawed logic and statistics, and significant performance costs). Our goal is to educate investors as to what these shortcomings are, why they exist, and suggest alternative approaches for measuring, monitoring, and potentially managing risk. In particular, we believe investors should decompose market prices into fundamentals and valuations. This model yields more insight into market dynamics and allows for more precise attribution of market performance. Here are three examples where this model can help investors measure, monitor, and potentially manage risk more productively:

- Invest more in stocks: We believe investors following our model will view market volatility differently. In particular, they may perceive stocks as being less risky than they would otherwise (using the traditional lens of volatility). All else equal[5], they may be inclined to allocate more to stocks. Even if one still follows a fixed asset allocation model, this could be an increase in one’s fixed stock allocation. Alternatively, one might choose to abandon the fixed allocation model and allow stocks to grow unconstrained. The higher stock allocation would likely result in more portfolio volatility, but investors would understand volatility itself does not constitute risk and be able to benefit from the higher returns over the long term.

- Avoiding emotional investment decisions: Filtering out market noise and focusing on more stable fundamentals can help investors remain objective by mitigating the emotions markets can stir (stress and anxiety during bear market periods and exuberance during bull markets). This objectivity can help investors avoid making very poor investment decisions (e.g., selling equities when prices are depressed or buying more after markets have rallied).

- Help investors make tactical decisions: Despite the negative stigma attached to market timing, market valuations are the key determinant of market returns over the long term. Much of this relationship is diluted by the many naïve valuation models being used in both academia and practice. Moreover, the results are mired in much short term noise. However, there are robust valuation models with 90% correlations to returns over longer periods (e.g., 10 years) and these can help investors improve performance and avoid enduring unnecessary volatility.

Is 100% stock allocation really that crazy? As long as one addresses their needs for liquidity (as to avoid extracting capital from the markets at bad times) and can tolerate the market price volatility, a 100% or near-100% allocation to equities is not as outlandish as one might suspect. Focusing on fundamentals and valuations instead of market prices should alleviate much of the unnecessary concern with market volatility. Moreover, if investors understand the costs associated with traditional asset allocation strategies, we suspect they will become more skeptical of their balanced portfolios – especially those with longer term investment horizon.

It is worth noting we are in good company in challenging the conventional definition of risk and the use of fixed asset allocation portfolios. Like many other great investors, Warren Buffett eschews Wall Street’s definition of risk. Moreover, his (i.e., Berkshire Hathaway’s) portfolio is virtually 100% stocks. We suspect he worked out the same math and logic we have here but long ago.

Unsurprisingly, we are often greeted with skepticism when we suggest higher equity allocations. In some cases (such as with retirees) we recommend a strategy whereby one reduces risk in their fixed income or bond allocations so that they can be less concerned with risk in other parts of their portfolio. For example, one can replace some are all of fixed income allocations with a basic annuity[6] to provide a fixed stream of payments. The annuity removes market and interest rate risk for this allocation because the payments are fixed and guaranteed by the insurer (and backed up by state insurance programs). Moreover, these payments can cover a significant portion of one’s monthly or annual retirement budget – perhaps covering essentials like food, shelter, etc.

Taking this approach one step further, one can allocate enough in one or more annuities (for diversification) so that the balance of the portfolio can be invested in dividend-paying stocks whereby the dividends alone cover the remainder of one’s retirement budgets. That is, they can live off of the dividends once a certain level of their budget is covered by the annuity product(s). Structuring a portfolio is this manner further reduces one’s dependence on the market. Even if one uses a broad market portfolio (e.g., S&P 500), the dividend stream is much more stable than market prices. In fact, one can invest in a portfolio of high quality dividend-paying stocks to mitigate dividend and market risk even further. We discuss this concept in our article Destroying Steady Income Streams.

| Note: Many investors and investment professional use various reported figures (e.g., earnings). These figures reported by companies follow GAAP[7] conventions and are for the IRS. That is, these figures are for accounting and may not necessarily reflect true fundamental performance. Moreover, companies can use financial engineering and manipulate their reported figures to a large extent. This is why we developed our own proprietary model for measuring and monitoring comprehensive fundamental performance. Feel free to contact us or visit www.FundamentalReporting.com to learn more about our model. |

Executive Summary

|

About Aaron Brask CapitalMany financial companies make the claim, but our firm is truly different – both in structure and spirit. We are structured as an independent, fee-only registered investment advisor. That means we do not promote any particular products and cannot receive commissions from third parties. In addition to holding us to a fiduciary standard, this structure further removes monetary conflicts of interests and aligns our interests with those of our clients. In terms of spirit, Aaron Brask Capital embodies the ethics, discipline, and expertise of its founder, Aaron Brask. In particular, his analytical background and experience working with some of the most affluent families around the globe have been critical in helping him formulate investment strategies that deliver performance and comfort to his clients. We continually strive to demonstrate our loyalty and value to our clients so they know their financial affairs are being handled with the care and expertise they deserve. |

Disclaimer

|

- 60% stocks / 40% bonds. ↑

- Notwithstanding our defense of deviating from fully-invested market portfolios, we do acknowledge the investment industry has diluted the market with many high-fee funds and strategies. Moreover, the managers of these funds often suffer from conflicts of interest relative to the goals of investors (e.g., job security encourages minimal deviation from industry benchmarks). You can do much worse that investing in a low-cost market portfolio. ↑

- This latter contention regarding timing the market is considered blasphemy amongst most advisors. We acknowledge market forecasts are worse than worthless in many cases. Moreover, even when one’s forecast is correct, there are practical considerations (e.g., taxes) that come into play. Notwithstanding, the historical evidence indicates there is much utility in some sensible long-term forecasting models and we believe they can be helpful even if only on rare occasions and for a minority of investors or investment professionals. ↑

- Readers interested in exploring tools based on quality and value can contact us for more information. Alternatively, we suggest reading the book Quantitative Value by Gray and Carlisle. They discuss and analyze a variety of models and show how integrating various value and quality metrics (both individually and together) has increased long-term returns and reduced portfolio drawdowns historically. ↑

- As highlighted multiple times in this article, we do not think all else is equal right now. In particular, we find valuations for the overall stock market to be elevated and expect low returns amidst much volatility. ↑

- Either the single premium immediate annuity (SPIA) or single premium deferred annuity (SPDA). In both cases, a lump sum of cash is translated into a stream of payments. These basic annuity products are typically competitively priced and reflect market interest rates (i.e., there is little embedded profit or commission). In general, we do not like many of the insurance and other commission-generating investment products being market to investors, but we believe basic annuity products like these can provide value in some circumstances. ↑

- Generally Accepted Accounting Principles ↑